How Students Are Using Digital Tools to Improve Financial Planning

The contemporary landscape of higher education is defined not just by academic rigor, but by an escalating economic paradox. Over the past two decades, the cost of attending a four-year institution in the United States has outpaced inflation, leaving the average graduate saddled with approximately $37,000 in student loan debt. Compounded by skyrocketing off-campus housing costs and everyday inflationary pressures, modern college students face an unprecedentedly complex financial environment. Survival in this landscape requires more than just part-time employment; it demands sophisticated, proactive asset management and budgeting systems.

Fortunately, the current cohort of higher education students—predominantly Gen Z and early Alpha—is uniquely equipped to combat these systemic macroeconomic challenges. As digital natives, these students are systematically turning toward advanced technological ecosystems to redesign their relationship with capital. From automated budgeting applications and algorithmic micro-investing platforms to AI-powered expense forecasting, technology has democratized access to fiscal literacy. Instead of relying on archaic Excel sheets or manual ledger entry, students are actively leveraging interconnected financial applications to achieve long-term fiscal stability while balancing heavy academic loads.

However, mastering these intricate digital asset management tools requires a fundamental grasp of foundational macroeconomic concepts, including compound interest, debt amortization, and localized tax structures. When academic schedules intensify, many scholars find themselves overwhelmed trying to analyze specialized financial metrics or complete complex corporate modeling projects. In such instances, obtaining expert structured guidance—such as professional help with finance homework—can bridge the gap between theoretical fiscal principles and their practical digital applications. This academic foundation ensures that when students configure automation thresholds in their fintech tools, they are backed by sound economic logic rather than arbitrary guesswork.

This comprehensive analysis explores the specific digital ecosystems students utilize to redefine financial planning, supported by empirical consumer data and institutional research.

Key Takeaways

- Fintech Proliferation: Over 70% of college students actively utilize mobile banking and dedicated neo-budgeting applications to track real-time expenses.

- Automation Over Manual Tracking: Automated savings rules and predictive AI expense categorization are replacing manual spreadsheets to reduce cognitive overhead.

- Micro-Investing and Fractional Assets: Fractional share investing platforms have lowered entry barriers, enabling students to participate in capital markets with minimal capital.

- Academic Synergy: Combining practical digital applications with deep theoretical comprehension is essential for long-term fiscal engineering.

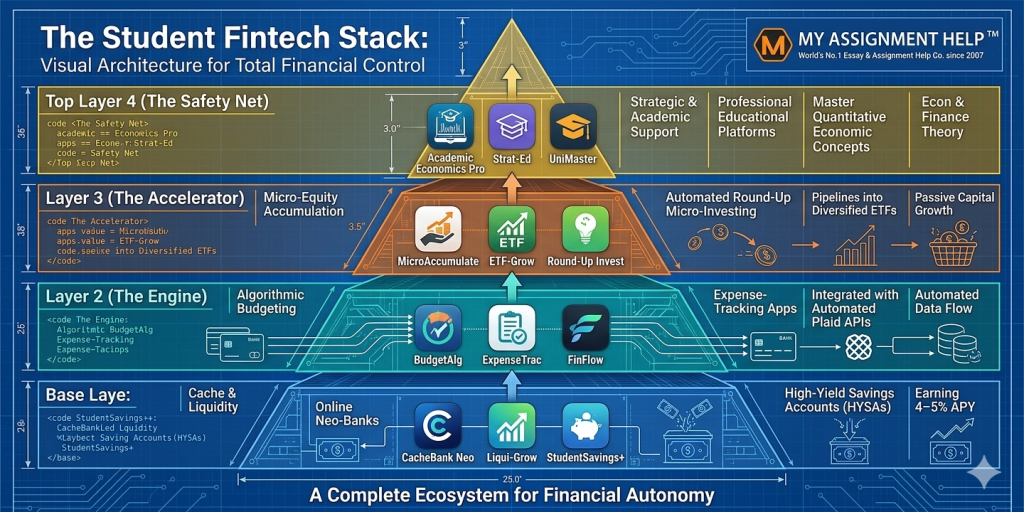

1. The Evolution of Student Budgeting: From Ledgers to AI Automation

Traditional budgeting metrics have historically relied on retrospective tracking—analyzing what was spent at the conclusion of a billing cycle. For a student operating on volatile, non-linear streams of income (such as seasonal federal work-study payouts, intermittent parental allowances, or gig-economy stipends), retrospective analysis is fundamentally flawed. It identifies fiscal deficits only after the capital has left the ecosystem.

Modern fintech applications address this vulnerability through real-time application programming interfaces (APIs) linked directly to student checking accounts via secure protocols like Plaid. Applications such as Rocket Money, Monarch Money, and YNAB (You Need A Budget) utilize predictive machine learning algorithms to categorize expenditures automatically. A transaction at a university bookstore is instantly logged under “Academic Overheads,” while a dining hall auxiliary charge falls under “Subsistence.”

More importantly, these tools utilize predictive cash-flow forecasting. By evaluating recurring fixed liabilities—such as monthly digital subscriptions, off-campus rent, and utility balances—against projected income intervals, the software generates a dynamic “Safe-to-Spend” metric. This cognitive offloading mitigates the “academic stress-spending” phenomenon, ensuring students do not inadvertently breach their baseline emergency reserves.

2. Micro-Investing Platforms and the Democratization of Capital Markets

Historically, entry into retail investment markets required substantial baseline capital, brokerage accounts with high minimum structures, and complex fee architectures. This effectively barred the student population from participating in compounding market returns during their prime formative years. Today, fractional share trading and automated micro-investing platforms have entirely eliminated these operational barriers.

Platforms like Acorns, Stash, and Robinhood allow students to convert marginal transaction variances into active investment capital. Through “round-up” algorithms, a student purchasing a laptop accessory for $42.30 can automatically redirect the remaining $0.70 variance into a diversified, low-cost Exchange-Traded Fund (ETF) or an index tracking the S&P 500. This automated dollar-cost averaging ensures that micro-incremental capital works continuously in the background without requiring active portfolio management.

According to data from the Financial Industry Regulatory Authority (FINRA), youth participation in retail brokerages has risen by more than 40% since 2021, with college-aged individuals citing accessibility and mobile user experience as primary catalysts. By engaging with these digital brokerages early, students gain exposure to risk-adjusted portfolio distributions, learning to navigate equity market volatility well before entering the full-time corporate workforce.

3. Neo-Banking, High-Yield Savings, and Liquidity Optimization

Traditional brick-and-mortar banking institutions have historically offered negligible interest rates on standard student checking and savings accounts, often hovering around a fraction of a percent (e.g., 0.01%). In an inflationary economic climate, capital held in these standard accounts rapidly loses purchasing power. Consequently, tech-savvy students are increasingly migrating toward digital-only neo-banks and online fintech ecosystems—such as SoFi, Ally Bank, and Wealthfront—to optimize their liquid cash allocations.

These digital banking institutions lack the heavy real-estate overhead of legacy banks, allowing them to pass savings back to consumers via High-Yield Savings Accounts (HYSAs) yielding upwards of 4.00% to 5.00% annually. For a student maintaining an emergency cash cushion of $3,000, shifting assets from a legacy commercial bank to a digital HYSA can generate significant passive returns over an academic year. Furthermore, these platforms feature granular internal “savings buckets” or digital vaults, enabling users to isolate funds explicitly for tuition installments, study abroad programs, or unexpected textbook expenses, ensuring absolute structural separation of operational funds.

4. Managing Debt Protocols and Credit Engineering via App Ecosystems

The handling of student loan debt and the establishment of a robust credit score are critical components of a student’s long-term financial health. A poor credit history or mismanaged student loans can restrict a graduate’s ability to lease apartments, secure auto financing, or access competitive interest rates later in life. Students are now turning to credit monitoring and debt optimization apps to build a strong financial foundation before graduation.

Applications like Credit Karma, Experian, and specialized student loan optimizers (such as Chipper) provide continuous visibility into credit metrics. Students use these tools to monitor their credit utilization ratios, track payment histories, and receive automated alerts regarding potential identity discrepancies. Many fintech platforms also offer student-specific credit cards that completely eliminate annual fees and reward responsible payment cycles with direct cash-back incentives or credit-limit extensions. By automating recurring micro-payments—such as a monthly phone bill—onto a student credit card and configuring an immediate auto-pay script from their primary checking account, students successfully build pristine credit profiles without taking on high-interest consumer debt.

Yet, managing these layered economic variables requires deep structural understanding. When balancing rigorous coursework alongside financial planning, academic execution cannot fall behind. Scholars struggling to balance corporate accounting modules or macro-econometric evaluations frequently rely on comprehensive educational services to manage their complex workloads. When a student requests an expert to help me with assignment tasks, they are optimizing their time. This strategic outsourcing allows them to protect their GPA while dedicating energy to managing their ventures, securing internships, and mastering real-world digital asset management tools.

5. Overcoming the Digital Pitfalls: Financial Literacy in the TikTok Era

While the proliferation of financial technology provides immense leverage, it also introduces clear consumer vulnerabilities. The democratization of investing has occurred alongside the explosive rise of financial influencer content (“FinTok”) across short-form video algorithms. Students are frequently exposed to high-risk, unverified financial advice, ranging from speculative cryptocurrency day-trading to highly leveraged options strategies and misleading multi-level marketing operations.

Additionally, the integration of “Buy Now, Pay Later” (BNPL) protocols—such as Klarna, Afterpay, and Affirm—into major e-commerce checkout engines presents a distinct risk to student cash flow. By breaking down a retail purchase into “four easy interest-free installments,” BNPL tools lower psychological barriers to spending. This often leads students to commit future unearned income to non-essential consumer goods, resulting in hidden debt accumulation.

To avoid these traps, students must ground their financial strategies in verified empirical principles rather than viral trends. Combining rigorous economic coursework with reliable digital tools helps students separate speculative internet hype from sound, long-term wealth accumulation frameworks.

Conclusion: The Empowered Digital Consumer

The modern college student is not a passive victim of macroeconomic pressures, but an active, technologically empowered financial manager. By integrating automated budgeting systems, utilizing high-yield savings repositories, deploying micro-investment strategies, and leveraging structured academic support networks, this generation is fundamentally changing what it means to be a student on a budget. As these digital tools continue to evolve with advanced generative AI features, the potential for personalized financial optimization will grow even further, setting up a new generation of graduates for lifelong economic stability.

Frequently Asked Questions (FAQs)

1. What are the safest digital budgeting apps recommended for college students?

Apps like YNAB, Rocket Money, and Monarch Money are highly recommended. For absolute beginners, platforms that utilize bank-grade 256-bit encryption and multi-factor authentication via Plaid are considered the safest choices for account integration.

2. How does an automated micro-investing app actually save money?

These applications work via transaction round-ups. If you buy a coffee for $3.50, the app rounds the purchase to $4.00 and automatically transfers the $0.50 variance into a pre-configured investment portfolio, allowing you to invest small amounts consistently without active effort.

3. Can digital tools help me manage and optimize my student loans?

Yes. Platforms like Chipper and specialized dashboards within your loan servicer’s mobile interface can calculate optimized repayment schedules, evaluate public service loan forgiveness (PSLF) pathways, and identify refinancing options to reduce lifetime interest costs.

4. Why are High-Yield Savings Accounts (HYSAs) superior to traditional college student savings accounts?

Traditional banks often offer interest rates as low as 0.01%, whereas online neo-banks offer HYSAs yielding between 4.00% and 5.00% because they don’t have the overhead costs of physical branches. This helps protect your cash savings against inflation.

5. Is it safe to link multiple financial accounts to a single dashboard app?

Most reputable fintech companies use Plaid or similar secure, read-only data transfer protocols. This means the app can view and organize your transactions but cannot execute transfers or alter your banking credentials, ensuring your funds remain secure.

About the Author

Dr. Marcus Vance, Senior Content Strategist & Academic Consultant Dr. Marcus Vance is a veteran financial analyst, educational researcher, and senior content writer at MyAssignmentHelp. He holds a Ph.D. in Consumer Economics from Ohio State University and has spent over a decade advising higher-education institutions on financial literacy curriculums. When he isn’t authoring deep-dive data analyses, Dr. Vance provides direct academic guidance to undergraduate and graduate scholars navigating the complexities of quantitative economic systems.

Data Sources & Empirical References

- Federal Reserve Bank of New York (2025): Quarterly Report on Household Debt and Credit, highlighting student loan trajectories and millennial/Gen Z debt obligations.

- Financial Industry Regulatory Authority (FINRA) Foundation Research: Empirical analyses tracking retail brokerage account creation and investment behaviors among young adult cohorts.

- National Center for Education Statistics (NCES): Long-term data evaluations mapping the true inflation-adjusted cost curve of higher education tuition in the United States.